I still remember the first small cap I ever made real money on. Barely anyone I knew had heard of it, and over two years it quietly tripled while the mega-caps everyone obsessed over went sideways. That taught me something I’ve never unlearned: the biggest percentage moves rarely come from companies already on magazine covers. So here’s the honest version up front. The best small cap growth stocks are companies with market caps roughly between $300 million and $2 billion, growing revenue fast — think 15% to 30%-plus a year — while attacking a large, expanding market with founder-level skin in the game.

That’s the profile. The catch is that this is the highest-risk, most volatile corner of the equity market, and you have to manage it like one. Below is the framework I wish someone had handed me twenty years ago — not a stock-tip list with a three-week shelf life, but a durable way to find these companies, judge them, and keep one bad quarter from blowing a hole in your account.

What actually counts as a small cap growth stock

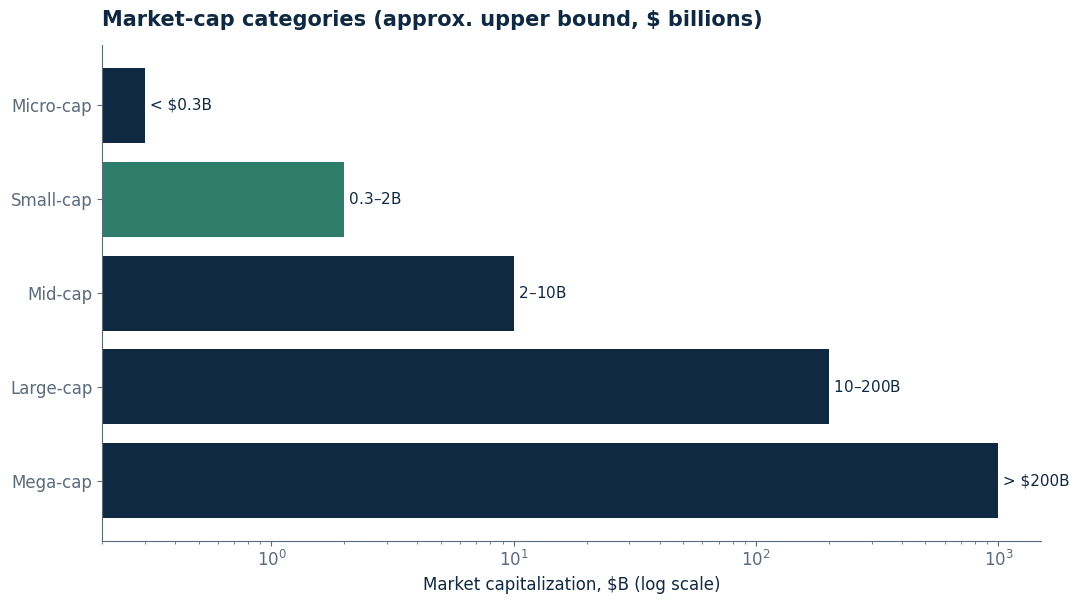

Let’s clear up the definition, because people throw “small cap” around loosely. Market capitalization is just share price times shares outstanding — the total value the market puts on the whole company. Small caps generally sit between roughly $300 million and $2 billion. Below that you’re into micro-cap and nano-cap territory, a different and frankly more dangerous game; above it you cross into mid-caps.

“Growth” is a separate filter stacked on the size filter. A small cap growth stock isn’t just any small company — plenty are slow-growing, sleepy, or quietly dying. The growth subset expands revenue and, ideally, earnings meaningfully faster than the market. In practice I want top-line growth comfortably in the double digits, and the ones that excite me most are compounding sales 25% to 40% a year off a small base.

Here’s what matters more than the numbers, though: stage. The small caps I want to own have proven customers will pay for what they sell — they’ve found product-market fit — but haven’t saturated their opportunity. They’re in the early innings, and the whole bet is the journey from scrappy niche player to category leader, because that transition is where the outsized returns get made. For the foundation underneath all of this, start with our broader guide to growth stock investing and come back for the small-cap wrinkles.

What I look for in a small cap grower

Over the years I’ve boiled my checklist down to the traits that actually move the needle. None of it is a magic formula — investing doesn’t have one — but when a company checks most of these boxes, it earns a spot on my research list. Here’s the table I run through in my head every time.

| What I look for | Why it matters | Rough benchmark I use |

|---|---|---|

| Revenue growth | The engine of everything; small bases can compound fast | 20%+ year over year, ideally for several quarters |

| Large, expanding market (TAM) | Determines how long the growth runway lasts | Company captures a small slice of a big, growing market |

| Gross margins | High margins mean growth can eventually fund itself | Strong or clearly improving over time |

| Path to profitability | Cash-burners get punished hard when sentiment turns | Profitable, or a credible, near-term path to it |

| Insider ownership | Founders with skin in the game think like owners | Meaningful collective stake (roughly 10%+ is a good sign) |

| Manageable debt | Heavy debt is brutal for small, volatile companies | Light balance sheet; no looming refinancing cliff |

| A real moat in the making | Something that stops bigger rivals from copying them | Switching costs, network effects, brand, or niche dominance |

If I had to rank these, revenue growth and market size come first — they define the upside. But profitability and the balance sheet keep you out of trouble. A small cap burning cash with no path to breakeven is a bet on the market staying generous, and it isn’t reliably generous. I’ve watched too many “story stocks” with gorgeous revenue charts get halved because they had to raise money at exactly the wrong moment.

Where small caps sit: the market-cap tiers

It helps to see the whole map, because “small cap” only means something relative to everything else. Companies get bucketed by market cap into tiers that each behave differently: mega-caps are the trillion-dollar giants, large caps the household names, mid-caps the still-growing middle. Small caps and micro-caps sit at the volatile, under-followed end — where the information edge is biggest and the risk highest.

I want to stress the word “typical.” These thresholds are conventions, not laws — different index providers draw the lines in different places, and the dollar figures drift over time as the market grows. Some definitions stretch “small cap” up toward $10 billion, which honestly blurs into mid-cap territory. Treat the buckets as a rough orientation and check how any given fund or screener defines things before assuming two sources mean the same thing.

Why does the tier matter so much for returns? Math. It’s far easier for a company doing $200 million in revenue to reach $400 million than for a $50 billion behemoth to reach $100 billion. The small company can double on a handful of big contracts, one new region, or a single hit product; the giant has to essentially re-create itself. That “smaller base, easier growth” reality is the whole reason small cap growth carries higher return potential — a durable structural fact, not a market-timing call.

Why small cap growth stocks can outperform

The long-run case for small caps rests on a couple of pillars that have held up across decades, even if no single year is guaranteed.

The size premium

Academics have long documented that, over extended periods, smaller companies have tended to outperform larger ones — the so-called “size premium.” Layer a growth filter on top and the potential outperformance can be even more pronounced. The adult caveat: this premium is lumpy and unreliable on any short horizon, with multi-year stretches where small caps lag badly. It’s a long-game phenomenon, and you only collect it if you can sit through the rough patches without panic-selling.

The inefficiency edge

This is the part I find genuinely exciting, and where a diligent individual investor can actually compete with Wall Street. A mega-cap tech company might have forty-plus analysts dissecting every comma in the earnings call. A promising small cap might have fewer than five — sometimes none. That coverage gap creates pricing inefficiencies. The market simply hasn’t done its homework on these names yet.

By the time a major bank initiates coverage and the media “discovers” a small cap growth story, the stock has often already doubled or tripled from where the early, patient researchers found it. You can’t get that edge in Apple or Microsoft — the whole world is watching. You can still get it in the under-followed corners. For the practical mechanics of spotting these companies early, I lean on the approach in our guide on how to find growth stocks before they explode.

How I actually find small cap growth stocks

Finding great small caps takes more legwork than picking large caps, precisely because the information isn’t handed to you. Here’s the process I run, in order.

Start with a screen

I start with a screener and a few non-negotiables: market cap in the small-cap range, year-over-year revenue growth above 20%, revenue rising for at least four straight quarters, and gross margins that are healthy or clearly improving. Depending on the cycle, that net pulls back roughly a hundred to a couple hundred candidates. The screen isn’t the answer — it’s the funnel. It tells me where to point my attention.

Size up the market they’re attacking

Next I look hard at the total addressable market, because for small caps the TAM determines how long the runway extends. A company doing $200 million in a $2 billion market has maybe 10x of headroom; one in a $50 billion market has vastly more. The best small cap growth investments grab a tiny share of a huge, expanding market. Limited TAM is a quiet way a growth story stalls — the company didn’t fail, it just ran out of room.

Read the business, not just the chart

This is where the real work lives. I read the actual 10-K and recent earnings transcripts to understand how the company makes money, who the customers are, whether revenue is recurring or lumpy, and what the competition looks like. Then one blunt question: why won’t a bigger, better-funded rival simply crush this company once it gets noticed? If I can’t name a defensible answer — switching costs, a network effect, a brand, real niche dominance — I move on. A great revenue chart with no moat is a trap.

Check who owns it

Insider ownership matters more in small caps than almost anywhere else. When founders and executives hold a real chunk of equity, their incentives line up with mine — they win when the stock wins, not just when they collect a salary. Executives sell for a hundred boring reasons, so selling tells me little. But cluster buying — several insiders putting their own cash in at once — gets my attention every time. Nobody knows the business better than the people running it.

The risks I never let myself forget

I’d be doing you a disservice if I made this sound like easy money. It isn’t. The same traits that give small caps their upside make them dangerous, and I treat the risks as the price of admission, not an afterthought.

Volatility. Small caps move. A missed quarter, a key customer loss, or just a sour macro mood can knock 20%, 30%, even 50% off one of these names fast. If a 40% drawdown would make you sell at the bottom, you’re not sized correctly for this asset class.

Thin liquidity. Fewer shares trade, so spreads are wider and getting in or out cleanly is harder — especially in a panic, which is exactly when you might want to move. I use limit orders, never market orders, on the thinner names.

Financing risk. Many small caps aren’t yet self-funding. When credit tightens, a company that needs capital can get forced into dilutive financing at a terrible price, hammering existing shareholders. A strong balance sheet is your protection here.

Concentration in any one name. Because the blow-up risk is real and idiosyncratic, position sizing is everything. I’d rather own a basket of researched small caps than bet the farm on one “sure thing” — in this corner of the market there’s no such thing. For the full playbook, our piece on risk management for growth stock investors is the most important companion to this article — read it before, not after, you start buying.

Where small cap growth tends to cluster

Small cap growth stories aren’t spread evenly; certain corners of the economy produce far more of them. Technology and software are the obvious hunting ground — high gross margins, recurring revenue, and the ability to scale to many customers without proportional cost. A lot of these names list on the Nasdaq, long home to younger, faster-growing companies. Healthcare and biotech throw off plenty of small caps too, though biotech is its own binary-outcome beast that I size extra small. Consumer brands occasionally produce a rocket when a product catches fire, and every so often an industrial or niche-services name quietly compounds for years while nobody’s watching.

One nuance worth saying out loud: today’s small cap tech grower is, if it executes, tomorrow’s mid-cap and eventually large-cap name. The biggest technology companies in the world were all small caps once. To study the established winners that started small, our roundup of the best technology growth stocks is a useful complement — same growth DNA, just further along the journey.

How I’d actually build a small cap growth sleeve

Let me get concrete about portfolio construction, because owning the right companies the wrong way still loses money. This isn’t personalized advice — just the sensible default I use myself.

First, small caps are a sleeve, not the whole portfolio — for most people they’re the high-octane satellite around a more stable core, not the foundation. Second, diversify within the sleeve. I’d rather hold a handful of researched names than one or two, because any single one can disappoint badly and I don’t want that to be fatal. Third, size each position so a brutal drawdown in any one of them is survivable and, frankly, boring. If one name going to zero would seriously hurt, it’s too big.

I also keep my time horizon honest. Small cap growth is a multi-year commitment — the thesis is that these companies grow into much larger versions of themselves, and that takes years and rarely moves in a straight line. If you find yourself checking quotes daily and reacting to every wiggle, you’ve picked the wrong strategy for your temperament, and that’s worth knowing before the money’s on the line. For individual ideas across the whole growth spectrum, I keep our list of the best growth stocks to buy in 2026 open alongside my own screens.

Small cap stocks vs small cap ETFs

You don’t have to pick individual names to get exposure here. ETFs like the Vanguard Small-Cap Growth ETF (VBK) or the iShares Russell 2000 Growth ETF (IWO) bundle hundreds of small cap growth companies into one ticker, which removes single-stock blow-up risk and asks nothing of you after the purchase.

The trade-off is familiar. A fund hands you the basket’s average outcome — no single position triples your money, but no single bad apple wipes you out either. Individual names offer a shot at real outperformance in exchange for research and far more volatility. What I do is run both: an ETF as the steady base, with a few individual names around it where I’ve done the homework and have real conviction. The fund carries the diversification; the individual picks supply the upside.

Common mistakes I see (and have made)

A few traps catch nearly everyone here, myself included over the years. Chasing the revenue chart while ignoring the balance sheet is the big one — a beautiful growth line means little if the company runs out of cash before it turns profitable. Confusing a low share price with a cheap stock is another; a $4 stock can be wildly overvalued and a $400 stock a bargain, because price per share tells you nothing without the share count behind it. Buying micro-caps thinking they’re “just smaller small caps” is a third — that tier is far riskier, thick with illiquidity and, at the bottom, outright promotion schemes. And the quietest killer: over-concentrating because a thesis feels obvious. The most obvious-looking bets are the ones I size most carefully.

Frequently asked questions

What qualifies as a small cap growth stock?

It’s a company with a market capitalization roughly between $300 million and $2 billion that’s growing revenue and earnings meaningfully faster than the broad market — typically double-digit top-line growth, often 20% to 30%-plus. The “growth” label separates these fast expanders from the many small companies that are slow-growing or stagnant. Always confirm how a given source defines the cap range.

Are small cap growth stocks riskier than large caps?

Yes, clearly. They’re more volatile, less liquid, more sensitive to interest rates and the economic cycle, and often more dependent on raising outside capital. That heightened risk is the flip side of their higher return potential. The way I handle it is disciplined position sizing, diversifying across several names, and committing to a multi-year time horizon rather than trading the swings.

How do I find the best small cap growth stocks?

Start with a screen for small market caps and revenue growth above roughly 20% for several quarters, then do the real work: read the 10-K and earnings calls, gauge the size of the market they’re attacking, check gross margins and the path to profitability, and look for meaningful insider ownership. The screen narrows the field; reading the business is what actually finds the winners.

Should I buy individual small caps or a small cap ETF?

Depends on how much time and risk you want. ETFs like VBK or IWO give instant diversification and no maintenance, at the cost of ever beating the basket. Individual names offer real upside but demand research and stomach for volatility. Personally I run both — a fund as the base, a few researched individual picks around it for the extra return potential.

Why do small cap stocks sometimes outperform large caps?

Two reasons. The long-documented “size premium” means smaller companies have tended to beat larger ones over long horizons, and small caps are under-covered by analysts, which creates pricing inefficiencies a diligent investor can exploit. On top of that, the simple math of growth favors small bases — doubling $200 million in revenue is far easier than doubling $50 billion. None of it is guaranteed in any single year.

The Bottom Line

Small cap growth investing is, to me, the most rewarding and most punishing part of the market — and those are the same fact. The upside comes from buying real, fast-growing businesses before the crowd notices, while they’re still under-followed and attacking a market many times their size. The danger comes from that same obscurity, thin liquidity, and financing risk. Get the company selection right, size positions like the volatile bets they are, diversify within the sleeve, and give your theses years rather than weeks. Do that, and the best small cap growth stocks can compound into a position you’ll still be telling stories about. Cut corners on the risk management, and this is the fastest way I know to lose money in growth. Respect both sides, and the math works in your favor.

Last updated: June 2026. Figures are approximate and change — confirm current data before investing. Educational only, not individual investment advice.